Home Equity Loans vs. Equity Loans: Recognizing the Differences

Home Equity Loans vs. Equity Loans: Recognizing the Differences

Blog Article

Trick Factors to Consider When Applying for an Equity Lending

When thinking about requesting an equity funding, it is essential to browse via different key aspects that can substantially affect your financial well-being - Home Equity Loan. Comprehending the sorts of equity finances offered, reviewing your qualification based on monetary variables, and carefully examining the loan-to-value ratio are necessary initial steps. The intricacy grows as you dive into contrasting rate of interest rates, fees, and settlement terms. Each of these aspects plays an important role in figuring out the overall cost and feasibility of an equity finance. By meticulously scrutinizing these aspects, you can make informed choices that align with your long-lasting financial objectives.

:max_bytes(150000):strip_icc()/home-equity-loans-315556_final3-23fa1237c577475f811fe9fc06eedec2.png)

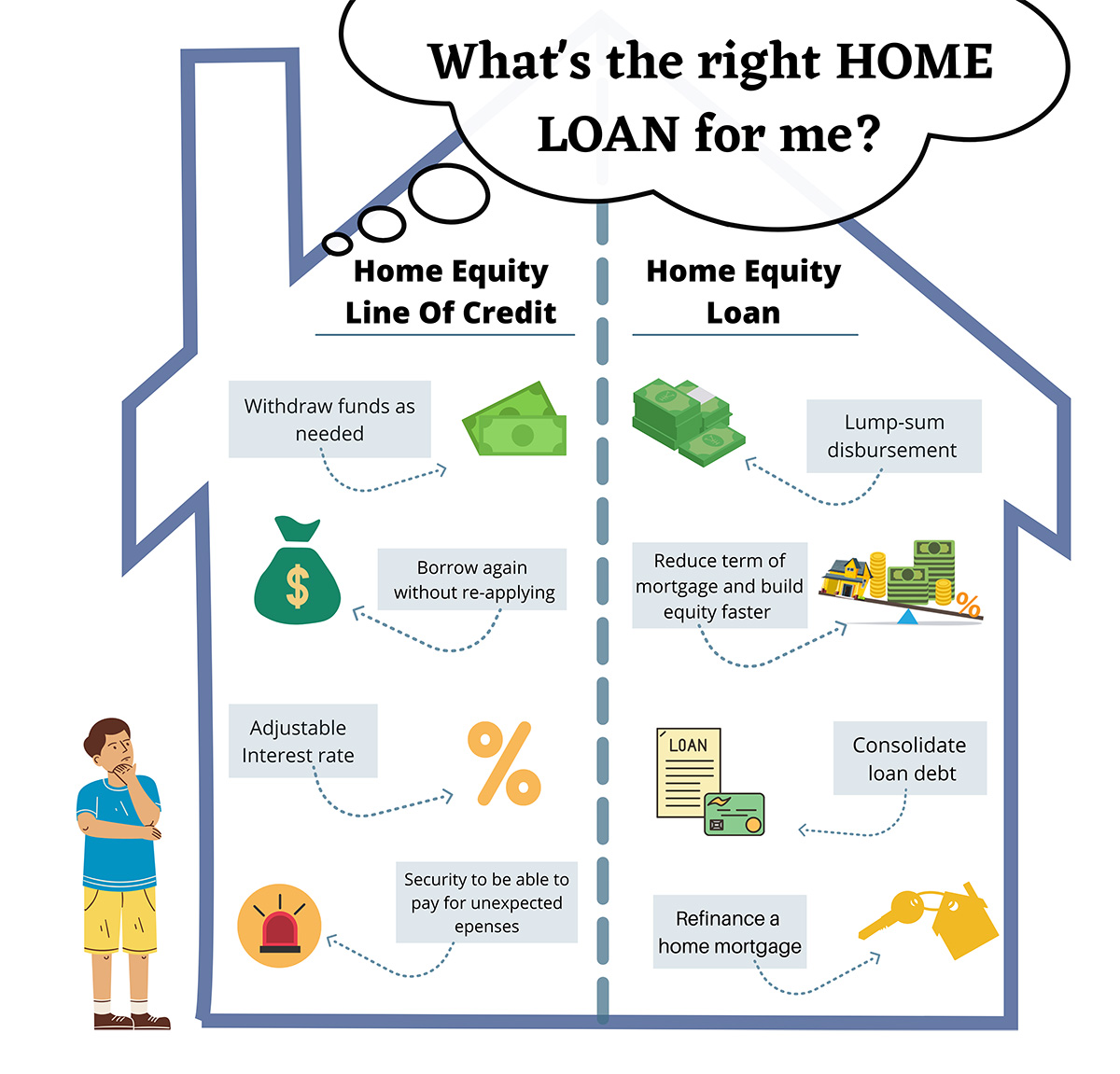

Sorts Of Equity Financings

Different banks offer a variety of equity lendings tailored to satisfy varied loaning requirements. One typical kind is the typical home equity finance, where house owners can obtain a lump amount at a set rate of interest, using their home as security. This kind of finance is ideal for those who need a large amount of money upfront for a specific function, such as home remodellings or debt loan consolidation.

An additional preferred option is the home equity credit line (HELOC), which works more like a bank card with a rotating credit history limit based upon the equity in the home. Debtors can draw funds as required, up to a specific limit, and just pay passion on the amount used. Equity Loans. HELOCs are ideal for continuous expenditures or tasks with unsure expenses

Additionally, there are cash-out refinances, where homeowners can re-finance their existing home mortgage for a higher amount than what they owe and obtain the distinction in cash - Alpine Credits Home Equity Loans. This kind of equity loan is useful for those looking to capitalize on reduced rate of interest or accessibility a large amount of cash without an additional regular monthly settlement

Equity Finance Eligibility Elements

When taking into consideration qualification for an equity financing, economic establishments generally examine elements such as the candidate's credit scores score, revenue stability, and existing financial debt commitments. Revenue security is another vital aspect, demonstrating the debtor's ability to make regular finance settlements. By thoroughly examining these factors, economic organizations can determine the candidate's eligibility for an equity financing and develop ideal lending terms.

Loan-to-Value Ratio Considerations

Lenders normally choose lower LTV proportions, as they offer a higher cushion in situation the consumer defaults on the loan. Debtors must intend to maintain their LTV proportion as low as possible to improve their possibilities of authorization and safeguard a lot more desirable lending terms.

Rates Of Interest and Costs Comparison

Upon analyzing interest prices and charges, debtors can make enlightened choices relating to equity financings. Interest prices can substantially influence the general expense of the financing, influencing regular monthly repayments and the complete quantity paid off over the finance term.

Other than interest rates, debtors should likewise think about the numerous charges connected with equity finances - Alpine Credits. These charges can consist of source fees, appraisal charges, shutting expenses, and early repayment charges. Source charges are charged by the lending institution for processing the funding, while appraisal costs cover the expense of analyzing the residential property's value. Closing prices include different charges connected to settling the loan agreement. Prepayment penalties may apply if the debtor pays off the car loan early.

Payment Terms Analysis

Efficient analysis of repayment terms is essential for borrowers seeking an equity funding as it directly affects the lending's affordability and economic outcomes. The lending term refers to the length of time over which the debtor is anticipated to pay back the equity funding. By completely assessing repayment terms, debtors can make enlightened choices that line up with their financial purposes and guarantee effective loan monitoring.

Final Thought

In verdict, when obtaining an equity loan, it is very important to think about the kind of finance offered, qualification variables, loan-to-value proportion, passion rates and fees, and settlement terms - Alpine Credits. By carefully examining these key aspects, borrowers can make enlightened choices that align with their economic goals and conditions. When seeking an equity financing., it is crucial to extensively research study and contrast alternatives to guarantee the ideal feasible end result.

By thoroughly examining these elements, financial institutions can determine the applicant's qualification for an equity lending and establish appropriate loan terms. - Equity Loan

Rate of interest prices can considerably affect the general cost of the financing, affecting monthly repayments and the total quantity repaid over the loan term.Reliable assessment of repayment terms is essential for customers seeking an equity finance as it straight impacts the lending's cost and financial end results. The funding term refers to the size of time over which the borrower is anticipated to repay the equity funding.In verdict, when using for an equity financing, it is essential to take into consideration the type of lending readily available, eligibility variables, loan-to-value proportion, interest rates and costs, and settlement terms.

Report this page